How to calculate futa tax

The Federal Unemployment Tax Act (FUTA) was established to provide unemployment benefits for workers who have lost their jobs. Employers are required to contribute to the program by paying FUTA taxes on the first $7,000 of each employee’s wages. In this article, we will guide you through the process of calculating FUTA taxes.

Step 1: Determine if You Are Liable for FUTA Taxes

Before calculating FUTA tax, ensure that your business is liable for it. You are liable for FUTA tax if:

-You paid wages of at least $1,500 to any employee during any calendar quarter of the current or previous calendar year, or

-You had at least one employee on any day of each of 20 different weeks during the current or previous calendar year.

Step 2: Identify Employees Subject to FUTA Taxes

Not all employees are subject to FUTA taxes. The following groups are typically exempt from these taxes:

-Independent contractors

-Certain family members of business owners

-Nonresident aliens with specific visas (e.g., F-1, J-1, M-1, Q).

Step 3: Calculate Employee Wages Subject to FUTA Taxes

The first $7,000 in wages paid to each employee in a calendar year is subject to FUTA taxes. Wages include salaries, commissions, bonuses, and other forms of compensation.

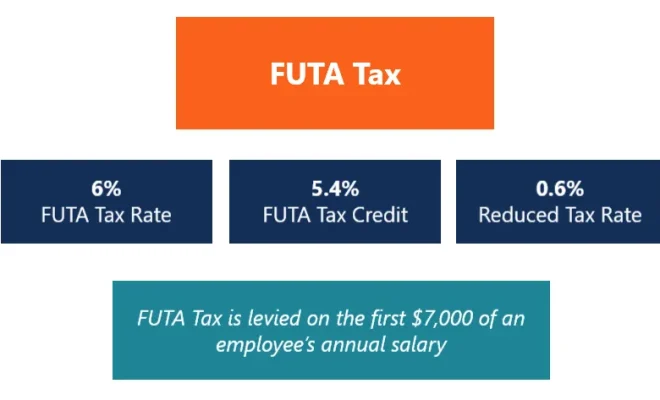

Step 4: Determine Your FUTA Tax Rate

The standard FUTA tax rate is 6.0%. However, you may be eligible for a credit reduction if your state has repaid loans from the federal government to cover their unemployment benefits program.

If your state is eligible for a credit reduction, you could receive a credit of up to 5.4%, reducing your effective FUTA tax rate to 0.6%.

Step 5: Calculate Your FUTA Tax Liability

To calculate your FUTA tax liability, multiply each employee’s wages subject to FUTA taxation (up to $7,000) by the applicable FUTA tax rate.

Example:

Assuming you have five employees with wages above $7,000, and your state qualifies for a credit reduction:

Total taxable wages = $7,000 × 5 employees = $35,000

FUTA tax liability = $35,000 × 0.6% (effective FUTA tax rate) = $210

Step 6: File and Pay FUTA Taxes

Employers are required to file Form 940 (Employer’s Annual Federal Unemployment Tax Return) annually by January 31st of the following year. If your FUTA tax liability exceeds $500 for a calendar year, you need to make quarterly deposits using the Electronic Federal Tax Payment System (EFTPS). If your liability is less than $500, you may carry it over into the next quarter(s) until it reaches this threshold.

Conclusion:

Calculating FUTA taxes is an important responsibility for businesses in the United States. By understanding the steps involved in determining employees’ taxable wages and identifying applicable tax rates, employers can ensure they meet their legal obligations and contribute meaningfully to the federal unemployment benefits program. If you need additional assistance with calculating FUTA taxes or filing your Form 940, consider consulting with a tax professional or payroll service provider.