How to calculate CVP

Cost-Volume-Profit (CVP) analysis is a crucial tool for businesses to understand the relationship between costs, volume and profit. It helps organizations to make informed decisions about pricing, production levels, and the potential for cost reduction. In this article, we will discuss how to calculate CVP and its benefits for your business.

Step 1: Understand the Components

Before calculating CVP, it is essential to comprehend its three main components: fixed costs, variable costs, and contribution margin.

1. Fixed Costs: These are the expenses that remain constant regardless of production or sales levels. Examples include rent, salaries, and insurance.

2. Variable Costs: These are expenses directly related to production or sales levels. Examples include raw materials, direct labor costs, and shipping fees.

3. Contribution Margin: This is the difference between sales revenue and variable costs. The contribution margin indicates how much money is available to cover fixed costs and generate profits.

Variable Cost Per Unit = Total Variable Costs / Number of Units

Step 2: Calculate Variable Cost Per Unit

To determine variable cost per unit, divide the total variable costs by the number of units produced or sold.

Variable Cost Per Unit = Total Variable Costs / Number of Units

Step 3: Calculate Contribution Margin Ratio

Contribution margin ratio indicates what percentage of each sales dollar represents profit after covering variable costs. Calculate it by dividing contribution margin per unit by selling price per unit or total contribution margin by total sales revenue.

Contribution Margin Ratio = Contribution Margin Per Unit / Selling Price Per Unit

Step 4: Find Break-Even Point

The break-even point is when total revenue equals total costs (fixed and variable), which means there’s no profit or loss. To calculate the break-even point in units, divide fixed costs by the contribution margin per unit. To find out break-even sales in dollars, divide fixed costs by the contribution margin ratio.

Break-Even Point (Units) = Fixed Costs / Contribution Margin Per Unit

Break-Even Point (Sales) = Fixed Costs / Contribution Margin Ratio

Step 5: Calculate Desired Profit Levels

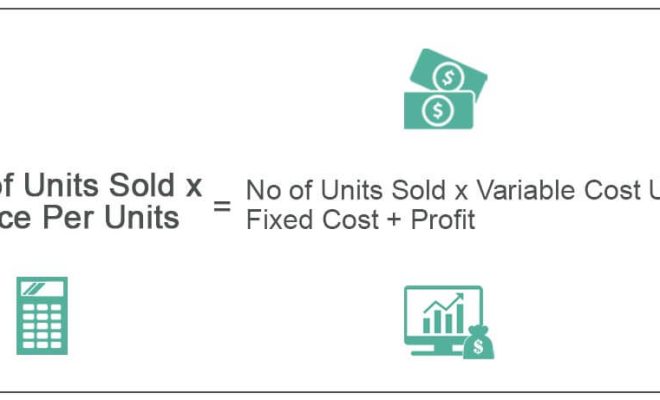

To determine the sales volume required to achieve a specific profit level, divide the sum of fixed costs and desired profits by the contribution margin per unit or contribution margin ratio.

Sales Volume (Units) = (Fixed Costs + Desired Profits) / Contribution Margin Per Unit

Sales Volume (Dollars) = (Fixed Costs + Desired Profits) / Contribution Margin Ratio

Conclusion:

Cost-Volume-Profit analysis serves as a vital tool for businesses, helping decision-makers forecast sales levels, understand price sensitivity and profitability. By calculating CVP, companies can make more informed decisions about pricing strategies, cost management, and production planning to ensure long-term success.